I don’t know why so many are caught up on the interest rate. You shouldn’t keep a balance on your credit card and should pay it off every month. No rewards card will ever come close to a good thing if you ever pay interest on it.

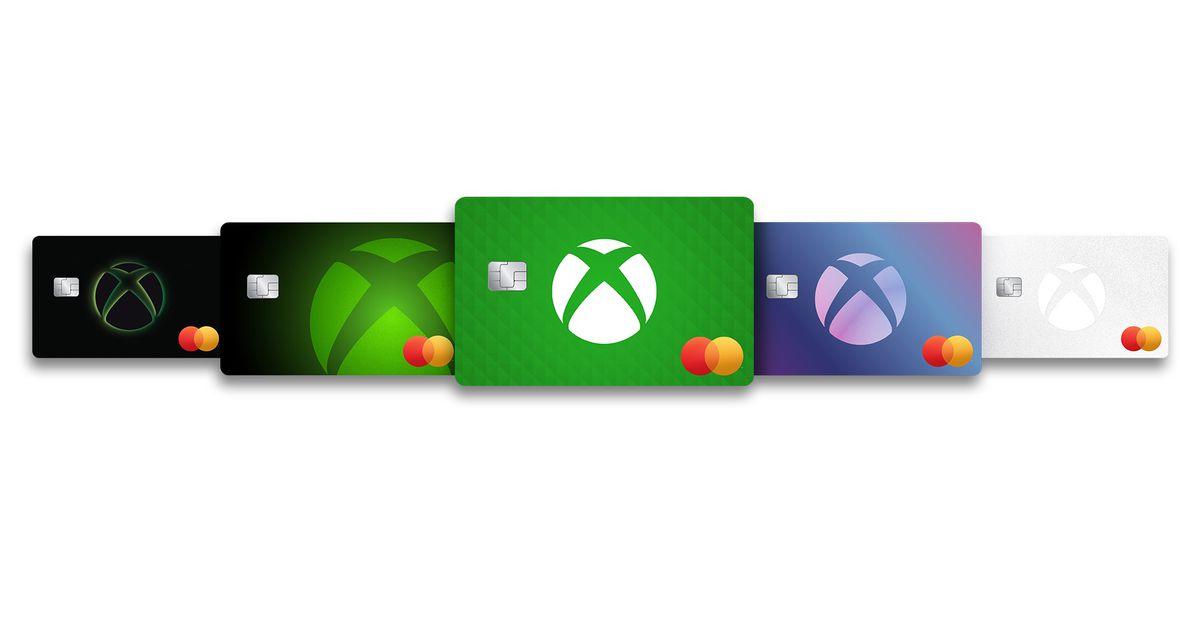

It’s also 5 points per dollar when spending at Microsoft, which is 5% back and a good deal. Majority of cards are 1% base with a bonus if you shop at their store. This card is pretty standard for the industry.

Doesn’t matter to me. I have like 10 different credit cards to get the best cash back depending where I’m shopping. Currently the best I get at Microsoft would be 2% so this is a pretty sweet card.

Credit scores usually go down with every new card you get, it only goes up when you’ve been stable with current card(s) (usually for, house etc (usually for 1-3 years range). Cause then they know you’re reliable with money in your current life situation.

Getting a new card will temporarily drop your score a few points.

If you’re like me that charges everything to a credit card, then you need a lot of available credit to keep the credit utilization low. You want it below 10%.

High credit utilization is going to drop your score more than opening a new card.

Say I have 1 card that has 15k limit. If I spend 10k on it. I have a 66% credit utilization. My score would be horrible.

Now, if I get 7 cards and each have 15k limits. If I spend 10k on them then I have less than a 10% credit utilization and my score would be good.

Can I get 1 or 2 cards that have credit limit of 105k. Yes. But I have found increasing limit is harder than getting a new card.

With a new card you can get 0% apr which is free borrowing of money for 12 to 15 months.

You can get a welcome bonus which are usually very good.

And you can set it up so that you might be getting more rewards like 5% cash back on dinning or other things that another card might not give.

Yes but if you need 1500 points at minimum before you can cash out, that means you aren’t seeing any cash back until you’ve spent $300 at Microsoft. The payout might be bigger, but you have to wait a lot longer to get it.

If that’s worth it for you, that’s great! But if I’m spend $60 at Microsoft a few times a year, I might rather just have $1.20 next month that I can spend on many things than $3.00 in two years that I can only spend at Microsoft.

21 to 32 percent APR is pretty standard for credit cards.

Which is why you should pay off the balance of a credit card each month where possible so that you accrue no interest, which can easily be done by setting up a direct debit. They’re not meant to be for long term borrowing.

Card companies will make their money from responsible users through merchant fees, which is them passing on the burden to merchants.

The main reason you’d want to use credit cards is for the added rewards and consumer protections you’d get.

Which is a convoluted way to say highly-restricted 1% cash back, which is pretty low-end these days, right?

At least 21% interest‽ I must be totally out of touch with the current reality, because that sounds outrageous.

I don’t know why so many are caught up on the interest rate. You shouldn’t keep a balance on your credit card and should pay it off every month. No rewards card will ever come close to a good thing if you ever pay interest on it.

It’s also 5 points per dollar when spending at Microsoft, which is 5% back and a good deal. Majority of cards are 1% base with a bonus if you shop at their store. This card is pretty standard for the industry.

deleted by creator

Doesn’t matter to me. I have like 10 different credit cards to get the best cash back depending where I’m shopping. Currently the best I get at Microsoft would be 2% so this is a pretty sweet card.

deleted by creator

You want a ton of cards to get good credit

5% is a lot bigger than 1%

Rewards add up

deleted by creator

My credit score is over 800 and I have 8 cards plus some store ones.

Getting more cards helps your credit score in the long run

No you don’t have to have a lot of cards to get a good credit score

But it does help

deleted by creator

Credit scores usually go down with every new card you get, it only goes up when you’ve been stable with current card(s) (usually for, house etc (usually for 1-3 years range). Cause then they know you’re reliable with money in your current life situation.

Getting a new card will temporarily drop your score a few points.

If you’re like me that charges everything to a credit card, then you need a lot of available credit to keep the credit utilization low. You want it below 10%.

High credit utilization is going to drop your score more than opening a new card.

Say I have 1 card that has 15k limit. If I spend 10k on it. I have a 66% credit utilization. My score would be horrible.

Now, if I get 7 cards and each have 15k limits. If I spend 10k on them then I have less than a 10% credit utilization and my score would be good.

Can I get 1 or 2 cards that have credit limit of 105k. Yes. But I have found increasing limit is harder than getting a new card.

With a new card you can get 0% apr which is free borrowing of money for 12 to 15 months.

You can get a welcome bonus which are usually very good.

And you can set it up so that you might be getting more rewards like 5% cash back on dinning or other things that another card might not give.

Getting more cards has it’s advantages

Good point, I’ll consider it in the future

Yes but if you need 1500 points at minimum before you can cash out, that means you aren’t seeing any cash back until you’ve spent $300 at Microsoft. The payout might be bigger, but you have to wait a lot longer to get it.

If that’s worth it for you, that’s great! But if I’m spend $60 at Microsoft a few times a year, I might rather just have $1.20 next month that I can spend on many things than $3.00 in two years that I can only spend at Microsoft.

Some people can’t do this or had an emergency and needed to use their credit card. Lower interest rates are manageable.

deleted by creator

Pretty easy to get a 2% card nowadays. This is a shit deal

My Apple Card gives me 1-3% depending on the purchase type. I average 2% since I use Apple Pay all the time.

21 to 32 percent APR is pretty standard for credit cards.

Which is why you should pay off the balance of a credit card each month where possible so that you accrue no interest, which can easily be done by setting up a direct debit. They’re not meant to be for long term borrowing.

Card companies will make their money from responsible users through merchant fees, which is them passing on the burden to merchants.

The main reason you’d want to use credit cards is for the added rewards and consumer protections you’d get.